Outline the key ways in which Consumers’ Behaviour differs when banking online and offline

Table of Contents

- Offline/Online Banking – What is it?

- Who’s Driving Online Banking?

- What are the Key Differences in Offline/Online Behaviour?

- Who is using Online Banking?

- Where is Online Banking Going?

- Can the banks operate equally?

- Conclusion – So what is the impact of this on the Consumer?

- Appendix

- Case Examples

- Example 1 – Savings Account Application.

- Example 2 – Online Credit Card Application.

- Example 3 – RaboDirect.ie.

- Example 4 – An independent third party.

Offline/Online Banking – What is it?

Put simply, it’s banking through the traditional bricks and mortar banking and banking on the World Wide Web. The world is changing, and it would appear that it is changing quickly. But why? Is it simply because we’re evolving faster online than expected? Or is it because we’re being forced online to stay out of the banks?

I would define the two different styles of banking as follow:

- Offline Banking:

- In branch banking;

- Telephone banking.

- Online Banking:

- Online accounts, such as Banking365 (BOI);

- RaboDirect.ie.

In this short paper I aim to explore several Consumer Behaviour Decisions/Theories which ask why people are shunning the traditional style of banking and are now moving to the web. For the purpose of this assignment I have interviewed several people and will be using both mine and their experiences to back up the points herein.

Who’s Driving Online Banking?

For this there are several theories. I would hypothesise that the Banks themselves are the biggest protagonists in the shift from the traditional to the digital. That is obvious in itself. However, what I think is not so obvious is that I believe they are using both direct and indirect means to force customers out of the branches and on to the computers. I think it may be fair to say that some banks are downgrading their services so much so as to make the experience in the bank so poor, that people will make the decision to migrate to online banking themselves. In essence, I believe banks are now making it increasingly difficult to stay in their branches. Example 4 in the Appendix would serve to reinforce this believe.

When I recently asked one person what they made of their most recent experience in a bank, I was met with this reply:

“You mean like the blank faces behind glass screens, with eyes devoid of sparkle, looking out at the winding queues? As you’re greeted with a heavy sigh, slumped shoulders and absolutely no eye contact whatsoever?

“Yes, a wonderful service. Mind you, I haven’t been in the IRBC at all. I’d say all those staff are literally laughing all the way to the *ahem* bank!”

Thus, with that in mind, one must ask oneself two questions:

i. Why would I keep going back into a bank when I’m clearly just a bank account number?

ii. Why are those staff members so unmotivated?

Both questions will inevitably lead to the customer doing the same thing. Ringing up the online bank services and setting themselves up online.

So, who is driving customers to online banking, and why? It’s the banks, clearly. And they’re doing it for one reason; to save money. But how are they doing it? I am of the opinion that they are doing this through direct and indirect methods. They are directly advertising the benefits of being online, hence the direct marketing bit. I also believe, however, that they are leaving their frontline staff in such a demoralised state that the customers in the queue are left with no recourse than to ask themselves the two questions, above.

Figure 1: An interviewee recalls a recent visit to a bank.

The banks themselves are also limiting exactly what the cashier and customer care representative can do for you. I recall one occasion where a bank clerk was going through a queue in a bank and asking the customers in the queue what their business was. Those who did not answer with “I’m looking for Currency Exchange” or “I wish to discuss a private matter” were met with “Did you know you can take care of that in our ATM’s” or “Did you know you can do that online? You can call up to register for banking 365.”. I asked myself at the time, does that clerk realise that they are slowly outsourcing their job?

Figure 2: A personal example of a recent experience in a bank.

It is, at the moment, in the banks interest to drive their customers to online banking. One could almost posit that the banks are diverting their budget for advertising in traditional banking to their advertising and marketing budget for online banking. If one was to observe the increase in services offered online, and the decrease in services offered offline, this of course makes sense. In addition to this, the major banks in Ireland are also continually decreasing their workforce and branch numbers.

What are the Key Differences in Offline/Online Behaviour?

Here are what I believe to be the key differences in the consumer mindset when it comes to Offline Banking -V- Online banking and how we perceive the experience:

| Offline Banking | Online Banking |

| Very little control;Little satisfaction;

The opening hours are very limited and inflexible; The personal interaction experience is gone; Frustrating experience. |

High rate of control;Ease of access;

24/7 service; No queuing; Very little interaction with Bank Employees. |

Bank Of Ireland also actively promotes their online services and their sites. As with any business, they are keeping up with web 2.0, but I think their long term strategy is to hold on to key locations and funnel customers through to their various sites. They are successfully taking advantage of the new founded innovative customer. Perception of service has led customers to expect more, and their expectations are being disappointed. The customer therefore now has no problem with becoming their own champion and finding their own answers.

The different brochures and advertisements are not telling people to call into a branch, but to go online or download the latest app. We are no longer able to be the 9-5 Monday to Friday society and this change reflects our new lifestyle.

So what’s the marketing strategy behind this? Simple, let the customers feel empowered. Get them the app, get them registered, get them doing everything for themselves. And why? It streamlines your business and, in theory, makes it easier to run and operate.

Who is using Online Banking?

Having conducted research into this from people across a wide age group, it would appear that it attracts nearly everyone. Those in their late teens to their later years are getting online. It seems to be growing alongside the rise of social media and with the evolution of the Internet. The gap between the elderly and the young online is closing. There are many attributing factors to coincide with this rise, of course. The biggest factor being that we are now, as a nation, becoming more PC friendly, and less tolerant of waiting. With this in mind the obvious conclusion is that we no longer like to wait for someone else, especially if we can take care of matters ourselves.

Where is Online Banking Going?

Online banking is managing to eliminate, one by one, the services offered in a branch. I have recently been able to open a savings account, successfully, and apply for another Credit Card online. Although there all still some kinks in the system, I believe that banks will attempt to follow the RaboDirect route and make traditional banking a thing of the past.

To aid this assignment I set myself three tasks to understand this further:

i. To open a savings account online;

ii. To apply for a credit card online;

iii. To open a RaboDirect.ie account.

Having recently been in a bank I decided that I was not going to put myself through the offline process again. Please see the appendix, under “Case Examples” for full cases.

Can the banks operate equally?

I would say no, they can’t. I would also say that all signs point towards them not wanting to operate a business model that allows people to do their business as easily offline as they can online. If one considers the banks own advertising, then we can see that they are constantly trying to get people to operate with a mouse and not with their feet. Simply put, in a world were the accountants are running the show, it makes fiscal sense. It no longer makes sense financially to provide the best customer service.

However, as one of my interviewees pointed out, there may be one saving grace.

Figure 3: Some people may just like the human interaction. If banks get rid of this, could they be cutting their long term sustainability?

As I stated at the start of this assignment we are now, as a people, evolving faster than we have done in the past. We are as likely to want a return to traditional banking as quickly as we are changing to online banking.

Conclusion – So what is the impact of this on the Consumer?

To conclude my input on this assignment I am going to suggest that the age of traditional banking is coming to an end. It is a simple fact that the experience has changed. It has been changed by the banks. It has been changed by our need for quick, efficient and effective service. It has been changed by our “I want it now” mentality. Change is natural, it happens with everything, but it happens faster now.

To quote another person I recently interviewed “If you could lodge cheques/bank drafts through some sort of serial ID process online, would that eliminate your need to go into a branch?” they responded with:

“Well, I also pay my bills through 365Online. It makes life handier than queuing all day. Not having to go to the bank is good simply because there’s not enough staff, and the one’s that are there don’t wanna be there.”

So, is it a case of us thinking that the banks don’t want us in there? We are very sensitive beings after all, subconsciously of course, and if we get the impression we’re not wanted we’ll go with that. And I think that may in fact suit the banks.

However, the reason the banks started increasing their online banking resources was to meet the demands that we, their customers, were demanding of them. We are no longer a 9-5 society, we are 24/7. We are switched on all the time. We sleep with our phones by our pillows. We wake up for emails. We need it now, tomorrow is no good. We are the now generation. We are the product of digital marketing and being able to literally have everything at our fingertips.

You may have noticed the lack of academic articles backing up this assignment. The reason I chose not to include any is simply due to the fact that there are none recent enough. This in itself shows the rapid rate of change in the subject matter.

Appendix

Case Examples

Example 1 – Savings Account Application

I logged into my account, as normal (a 3 click process) and set about finding the relevant tab to use. This was quite simple and very straightforward. I had my account set up and ready to go in minutes. Overall, this was a good experience. There was only interaction with the site, there was no person to person interaction.

Example 2 – Online Credit Card Application

Again, I logged into my account and found the relevant tab. After a few bits of clicking I was logged out and taken to the main Bank of Ireland site to apply for the “Clear Credit Card”. Here I had to answer a lot of questions, all on different pages. I was getting quite bored at this point and had it not been for this assignment I would have given up, and I certainly wouldn’t have gone into the bank looking for the application form. Finally, I got to the end. I was informed I would receive a phone and letter in relation to my application. The phone call came a week later and the letter has yet to arrive.

The phone call really made the whole experience. I missed the call, as I was in work. I was advised by the voicemail the representative left to call 1890-365-100 and ask for “Margaret”. This was ambiguous to say the least. I decided to return the call on my lunch break. I had to sift through the automated menu. There was no help number for phoning Margaret back. There was no “If you missed a call from Margaret, please press 9”. I kept on hitting numbers until I got to a person, a real person. Finally, I asked someone about Margaret, 15 minutes later. Strangely, they knew her. I was transferred.

At this point I must stress that I don’t even want this card anymore, but I’m stubborn, so I persevere. At last, the elusive Margaret. So what’s the news? The application has been approved, but I’ll have to give up my current card and transfer the balance to this one. What are the benefits of that, I ask. Well, it’s a lower credit limit and higher repayment rates, but somehow that is better for me and I should go for it. This is not making sense to me, so I ask again. All Margaret can tell me is that it’s better and that I should go for it. I don’t argue, I don’t point out the obvious flaw in her argument, I simply say Thank You, politely decline the offer, and carry on.

This sort of sums up Bank of Ireland at the moment. The way they are operating is not really better for us, but they’ll tell us it is, and expect us to believe them.

Example 3 – RaboDirect.ie

This was very straight forward, the only issue I have at the moment is that I have to send in supporting documentation to finalise the opening of my account. Unfortunately I have not done this as yet. The reasons for this are simple, I have to do a bit of offline work, and I haven’t been able to allot the time for this. It is unfortunate that I still have to rely on the 9-5 clock of other businesses to help me with this.

Example 4 – An independent third party

The following is an exact extract from an interviewee. It centres around their experience applying for a savings account and a credit card.

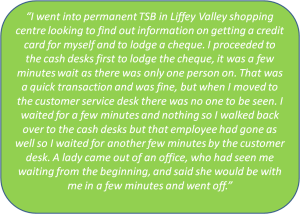

“I went into permanent TSB in Liffey Valley shopping centre looking to find out information on getting a credit card for myself and to lodge a cheque. I proceeded to the cash desks first to lodge the cheque, it was a few minutes wait as there was only one person on. That was a quick transaction and was fine, but when I moved to the customer service desk there was no one to be seen. I waited for a few minutes and nothing so I walked back over to the cash desks but that employee had gone as well so I waited for another few minutes by the customer desk. A lady came out of an office, who had seen me waiting from the beginning, and said she would be with me in a few minutes and went off. When she came back she invited me into the office to talk about the information. I asked if I could get info on getting a credit card. She asked if I had full time employment, I said no, I have part time employment. She asked how long I have been working there, and what my wage was a month. I answered, only since April as I was let go in my previous job, and I would get roughly €800 a month. According to what she looked up on the computer, I would need to be making a minimum of €1000, I would need to be in that job for at least 2 years, and have all my wages going into that account for the 2 years also. I am currently getting the wages into a different account but wanted to swap it over, but was told that I wouldn’t be able to qualify for a credit card at all and that was the end of the conversation, she just apologised. There was no effort to make sure I still swap my money into there account or anything.

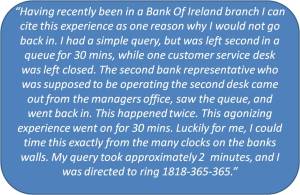

“On a separate day, I wanted to check if my cheque had cleared but the queue was very long at each of the machines as well as the cash desks. I waited at one of the machines and checked my balance but it hadn’t cleared yet. I wanted to find out when it would, as I needed the money but the queues were way too long so I left. Later that day I phoned up the help line and they transferred me to an operator, he was quite helpful and efficient and gave me the information I needed. He also asked if i needed help with anything else.

“In Ulster Bank in Liffey Valley, I asked for information on a credit card the same way as in Permanent TSB. Straight away I was brought into a room to discuss it. They have a set of forms to fill out to see if you qualify, he helped me fill out the forms, told me what extra paperwork I needed to put with it and when I brought the paperwork in he submitted them for me. I then received a letter in the post saying that I do qualify for a credit card and would I like to proceed in getting one. Not long after, I had my credit card ready to use.

“I applied online for a savings account with Ulster Bank, it was very simple and easy to follow. There were lots of different types of savings accounts that you can set up, but they have all of them broken down into important bullet points on all of them and you can click to view all the details if you wish. It took 5 minutes to complete the application and submit it.

Leave a comment